by Gkotsi Jenny

Journalist and Author

According to projections by the World Bank, global economic growth in 2025 is anticipated to slow to its weakest pace since 2008, excluding periods of crisis. This deceleration is largely driven by escalating geopolitical uncertainties and intensifying trade frictions, which are significantly undermining global economic momentum. As a result, investor confidence is waning, leading to constraints on both capital flows and consumer spending. A comprehensive analysis of the elements that shaped this situation enhances our understanding of the current landscape and informs projections for the future. A thorough examination of the various economic factors enables a clearer understanding of the underlying issues and allows for informed projections of potential outcomes. This analysis not only highlights the immediate challenges but also underscores the importance of strategic responses to navigate the complexities of the economic landscape ahead.

Global Εconomic Τrends

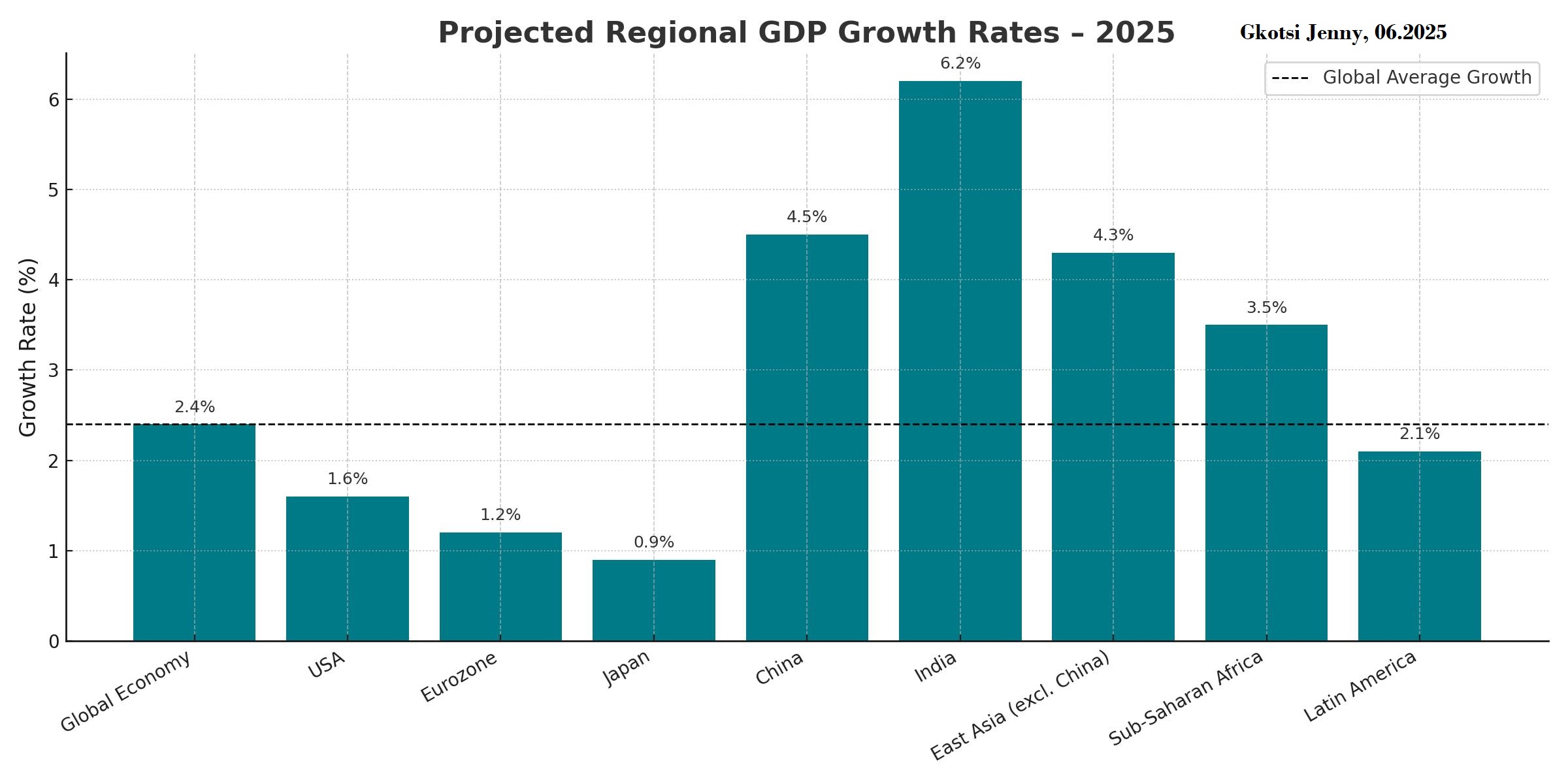

According to estimates from the World Bank and the International Monetary Fund, the global growth rate is expected to be around 2.4% in 2025, down from 2.6% in 2024. Developed economies are projected to experience a growth rate of less than 1.5%, with the U.S., Eurozone, and Japan showing signs of fatigue. In contrast, emerging markets present a slightly better outlook with a growth rate of approximately 3.9%, although there are significant disparities; countries like India and Indonesia are demonstrating strong growth, while China is showing weaker results.

Diagram 01: Projected Regional GDP Growth Rates 2025 (Gkotsi Jenny, 06.2025)

Factors that impede Economic Growth

- High Interest Rates:

The current policy interest rates of the central banks as of June 2025 are as follows: The Federal Reserve has maintained the Fed Funds target range at 4.25–4.50%. The European Central Bank recently reduced its deposit facility rate to 2.00% (ECB, 2025). Meanwhile, the Bank of England has kept its rate steady at 4.25% (Bank of England, 2025). These central banks, including the Fed, ECB, and BOE, keep interest rates elevated due to concerns about persistent inflation. The policy of high interest rates has serious consequences for the labour market, creating a “boomerang” effect that negatively impacts the economy. Increased borrowing costs restrict economic growth and lead to reduced investments. As a result, businesses are hesitant to hire or may resort to layoffs. Wage stagnation and rising unemployment limit labour mobility, while sectors dependent on borrowing, such as construction and services, are hit hardest. This results in fewer job opportunities and a decline in economic well-being.

2. Trade Tensions:

Escalating trade tensions among major global economies, most notably the United States, China, and the European Union, have introduced significant headwinds to international economic activity. The imposition of tariffs, export controls, and policies focused on economic security has led to the fragmentation of global supply chains, increased production costs, and reduced incentives for foreign direct investment. This environment of heightened uncertainty is constraining global trade flows and prompting firms to reassess their existing production and sourcing strategies, with potential long-term implications for globalisation.

3. Political Uncertainty:

The global political landscape remains highly volatile, as a series of major elections, including those in the United States, the European Union, India, and Mexico, introduce policy unpredictability and often delay structural reforms. Concurrently, the ongoing war in Ukraine and the escalating tensions between Israel and Iran have intensified geopolitical instability. These developments contribute to elevated levels of uncertainty, undermine investor and business confidence, and may hinder coordinated international responses to shared economic challenges.

4. Slowdown in China:

China, once a key driver of global demand, is now experiencing sub-5% growth—a notable deceleration relative to its historical performance. Structural challenges such as a protracted real estate crisis, demographic decline, and increasing constraints on private enterprise are eroding business confidence and undermining the country’s growth potential. These headwinds carry broader implications for emerging markets and global supply chains, given China’s central role in the world economy.

Ιmpacts of Εconomic Slowdown

1. Businesses:

Based on the Q2 2025 CEO Economic Outlook Index data, the sharp 15-point decline in the Business Roundtable CEO Economic Outlook Index to 69, its lowest level since 2020, underscores a growing sense of caution among corporate leaders. The marked deterioration in all three subcomponents reflects a widespread reassessment of the business environment: the 19-point drop in hiring plans suggests weakening labour demand, potentially signalling slower job creation in the second half of 2025. Similarly, the 15-point decline in capital investment intentions indicates that firms are pulling back on expansion and modernisation initiatives, often a sign of diminished confidence in medium-term economic growth. The fall in sales expectations, though less dramatic, confirms that revenue forecasts are being revised downward, likely due to concerns about consumer demand, trade barriers, and persistent inflationary pressures. Overall, the data point to a cautious corporate sector bracing for a potential slowdown, with significant implications for investment, employment, and GDP momentum in the coming quarters. In addition, Andrew Bailey (Bank of England, 2025) addressed critical themes affecting the global business environment as of May 2025, he stressed the necessity for careful management of interest rates to navigate inflationary pressures while fostering economic growth, emphasizing that maintaining price stability is essential for effective business planning and sustaining consumer confidence in the market.

2. Consumers:

According to the University of Michigan’s Surveys of Consumers, the Index of Consumer Sentiment in April 2025 remained well below its historical average, registering around 70–75, compared to a long-term norm of 85–90. This muted level of confidence mirrors conditions seen during major periods of economic strain, such as the early 1980s recession and the 2008 global financial crisis. While some indicators point to macroeconomic stabilization, ongoing concerns over inflation, geopolitical uncertainty, and household financial pressures continue to weigh heavily on consumer sentiment. Furthermore, higher payroll tax contributions in the UK, such as the increase in National Insurance rates introduced in 2022 and maintained through 2024, have reduced net household income, limiting consumption potential and dampening retail activity (Office for Budget Responsibility, 2024). In parallel, the U.S. has maintained elevated import tariffs on key consumer and intermediate goods, particularly those from China and the EU, which have raised production costs and consumer prices (U.S. Trade Representative, 2025). These measures have functioned as indirect consumption taxes, disproportionately impacting lower- and middle-income households (OECD, 2024). As a result, real purchasing power has eroded across both economies, contributing to persistently weak consumer sentiment, as reflected in recent data from the University of Michigan and GFK Consumer Confidence indices (University of Michigan, 2025; GfK, 2025).

3. Governments:

Fiscal buffers in many economies are now substantially eroded. According to the International Monetary Fund (IMF, 2025), global public debt is projected to reach 95% of GDP in 2025, with the ratio expected to approach 100% by 2030, indicating a shrinking margin for fiscal intervention. Empirical evidence suggests that countries with constrained fiscal space tend to adopt procyclical austerity measures during economic downturns, actions that can amplify rather than mitigate the contractionary effects of recessions (ADB, 2025). In the United Kingdom, fiscal strain is already evident: the Confederation of British Industry (CBI, 2025) forecasts stagnant growth due to rising trade barriers and increased payroll taxation, while limited budgetary flexibility leaves policymakers with minimal scope for discretionary fiscal stimulus.

Forecast

Forecasts indicate that the global economic recovery is unlikely to follow a “V-shaped” trajectory (Wu, 2024). Instead, the economy is expected to enter a prolonged phase of low or stagnating growth, resembling stagflation, unless there is a significant shift in critical policy and investment areas. To avert this scenario, coordinated global policy actions are essential, including large-scale investments in infrastructure and the transition to green energy. Additionally, there is a pressing need for accelerated technological investments, particularly in artificial intelligence and clean energy innovations. Furthermore, restructuring global supply chains will be crucial to enhance resilience and efficiency in an increasingly fragmented trade environment.

Thus, uncertainty continuously ignites a tendency for heightened economic tensions, often manifesting through political disputes within the framework of geopolitical differences. These tensions are intricately woven together by the underlying pressures of a profound economic crisis, which not only exacerbates conflicts but also complicates the resolution of related issues. The complex interplay of these factors renders the situation increasingly critical, necessitating strategic approaches to effectively address them.

References:

- ADB (2025) Asian Development Outlook: Fiscal Policy Under Pressure. Manila: Asian Development Bank.

- Bank of England (2025) Monetary Policy Summary – June 2025. London: Bank of England.

- Business Roundtable. (2025) CEO Economic Outlook Index: Q2 2025. [online] Available at: https://www.businessroundtable.org/media/ceo-economic-outlook-index/ceo-economic-outlook-index-q2-2025

- CBI (2025) Economic Forecast: Spring 2025 Update. London: Confederation of British Industry.

- ECB (2025) Monetary Policy Decisions – June 2025. Frankfurt: European Central Bank.

- GfK (2025) UK Consumer Confidence Barometer: April 2025. London: Growth from Knowledge.

- IMF (2025) Fiscal Monitor: Balancing Risks. Washington, D.C.: International Monetary Fund.

- OECD (2024) Economic Outlook, Volume 2024 Issue 2. Paris: Organisation for Economic Co-operation and Development.

- Office for Budget Responsibility (2024) Economic and Fiscal Outlook – March 2024. London: OBR.

- University of Michigan (2025) Surveys of Consumers: April 2025 Final Report. Ann Arbor: U-M Institute for Social Research.

- U.S. Trade Representative (2025) Trade Policy Agenda and 2024 Annual Report. Washington, D.C.: Executive Office of the President.

- Wu, Z., 2024. The “V-Shaped” Evolutionary Trajectory of Modernization in Modern and Contemporary China. In The Theory of Chinese Modernization (pp. 71-141). Singapore: Springer Nature Singapore.